There world of alternatives is fascinating. As I’m writing this, crypto has had an incredible year after a terrible 2022. The private equity world is…chugging along? From what I can gather, private credit seems to be taking the spotlight as LBO transactions decrease in a higher rate environment than we’ve seen in a while. If you trust the hedge fund indices from sources like Eurek Hedge and Barclays have probably had mid to high single digit returns. But an alt that has caught my attention in recent years is the less talked about “natural capital” side of things.

More specifically, I’m talking about private farmland and agriculture investments. One of the best sources I’ve seen on the topic is Nuveen; a large manager of natural capital that invests globally. Let’s get right into it.

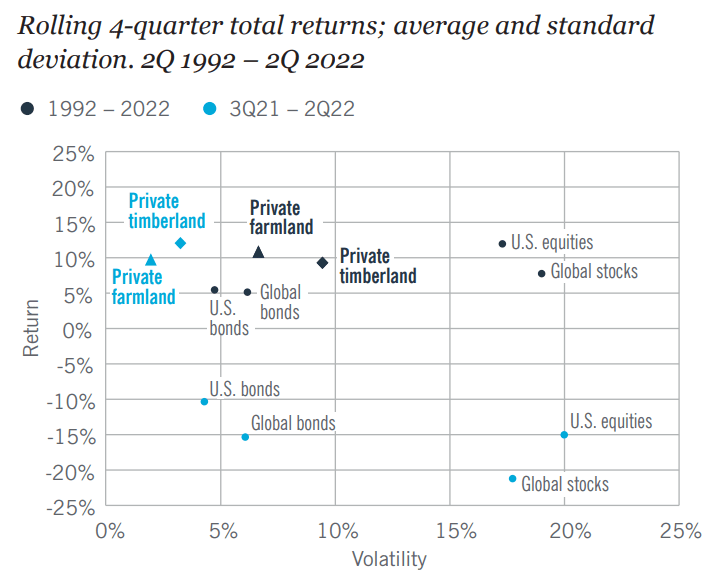

Natural capital investments have had strong returns over the past few decades.

Here’s a screenshot taken from Nuveen on the performance of natural capital over the years.

Fascinating. Performance similar to equities with much lower volatility. Now, I wouldn’t put too much weight on the volatility numbers here since the source of this data is NCREIF which is only updated on a quarterly basis. This leads to the same understatement of volatility that you’d find in any private equity index.

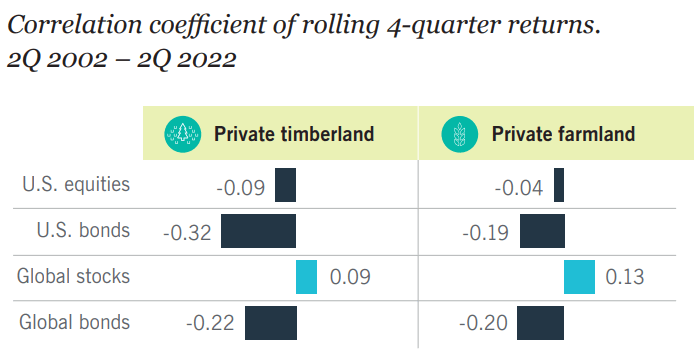

However the correlations of natural assets to traditional assets are so low that there seems to be a significant, if somewhat imprecise, diversification effect.

Here’s another screenshot from that Nuveen paper (I wish I had access to NCREIF natural capital data myself but alas). This is more or less uncorrelated to traditional assets.

I think a lot about diversification. Increased globalization over the course of the last few decades has, in my opinion, resulted in a lack of diversification from geography alone. Think of any company in the S&P 500; what share of its profits come from international markets compared to 1970? I’d make the same observation about companies in Europe and Asia. Normative judgments about globalization aside, finding things that are truly uncorrelated to public equities isn’t all that easy. Maybe the current anti globalization wave might have some impact on that over the next few years, but private timberland and farmland almost seem like low hanging fruit.

These are meaningful differences between timberland and farmland, and within them as well, that contribute to portfolio diversification.

The “cash flows” from timber and farmland come from the yields that they produce. Wood in the case of timber and crops from farmland. This means that they’re inherently subject to the volatility of the commodities markets. Harvests can be difficult to store for long periods of time, so low prices of a crop in a given year can mean lower yields than usual. There is also a wide variety of crops, so a diversified farmland portfolio can potentially have benefits.

You tend to have more flexibility when it comes to chopping down timber since you can hold out until timber prices recover without the risk of trees going bad like crops. But there is also some level of diversification within timber markets. Costs of transporting timber can be high given how heavy logs are, leading to regional markets and some degree of diversification.

There’s a ton more I can cover on sustainability and the specifics of timber/crop varieties but I’m out of time for now.

DISCLAIMER: I am not a financial advisor. Nothing on this website is to be constituted as financial advice. All content here is solely for educational purposes. They solely represent the opinion of the author.